- The top economic goal of the Trump administration is to boost the U.S. economy through changes in the tax code and diminished regulations. While economic growth has accelerated, the importance of regulatory changes often is downplayed by economists because it is difficult to quantify the overall impact.

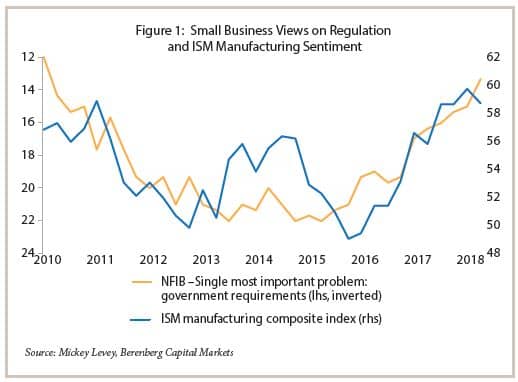

- Survey results for businesses — especially smaller firms — suggest regulatory changes are having some impact nonetheless: As shown in Figure 1 below, there is a link between the way small businesses view regulations and improvements in manufacturing sentiment.1 This is consistent with research that shows the impact of government regulations is greatest on small size firms.

- The environment is an extensive area of regulations to deal with externalities such as pollution. However, several studies suggest environmental regulations have become overly complex, and market-based solutions offer a more effective means for dealing with the problem of acid rain. Although several former Republican policymakers have proposed a carbon tax to combat global warming, President Trump believes the costs are too great for the economy.

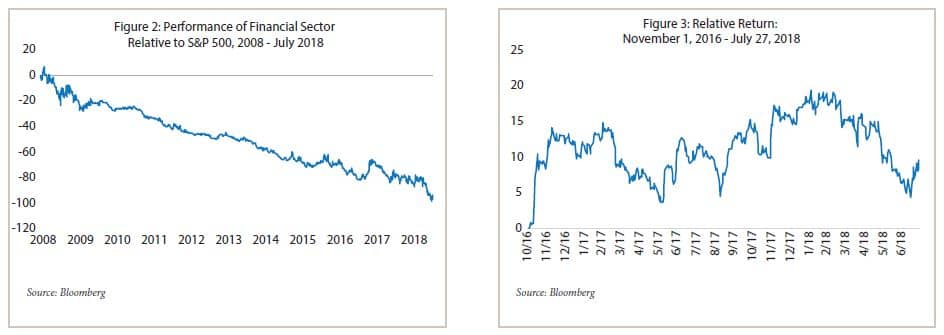

- Another important area is financial services, where the principal challenge is to ensure stability without turning banks into quasi-utilities. It is too early to ascertain the impact of policy changes to lessen the impact of Dodd-Frank, but financial stocks have matched the overall stock market for the first time in several years after trailing the broad market consistently since 2008.

Background: The Case for Deregulation

One of the most controversial issues in public policy relates to the role of government regulation of the economy. This is an area in which many businesses have expressed frustrations over the past two decades. In a speech to the Economic Club of New York shortly before the November 2016 elections, Donald Trump mentioned that he frequently asks CEOs what they would pick if forced to choose between tax cuts or diminished regulations. According to him, nine out of ten executives would opt to have fewer regulations. The reason: companies can hire tax experts to navigate their way around the tax code, but it is more difficult to circumvent regulations.

The regulatory burden is especially problematic for small businesses because the rules cause them to incur fixed costs, and the scale of operations is much smaller than for larger firms. For example, a study by Nicole Crain and Mark Crain of Lafayette College estimates the cost per employee of complying with federal regulations at $10.6 thousand for businesses with fewer than 20 employees compared with $7.8 thousand for those with more than 500 workers.2 The researchers also contend that government regulations make small business less competitive against foreign firms.

Nor does the United States fare well when compared with many industrialized nations. A study by the Organization for Economic Cooperation and Development (OECD) undertaken a decade ago found the U.S. barriers had higher regulatory barriers to entrepreneurship, greater administrative burdens on small business owners, and higher barriers to competition than a number of other industrialized countries. An article in The Economist titled “Over-regulated America” (February 18, 2012) made the following observation:

Americans love to laugh at ridiculous regulations…But the red tape in America is no laughing matter…Americans are supposed to be free to choose for better or worse. Yet for some time Americans have been straying from the ideal.

How Costly Are Regulations?

This begs the question about how costly regulations are for the economy as a whole. The problem is no one really knows.The federal government is not required to track regulatory costs, and most empirical studies have focused on a narrow set of industries. Federal agencies are only required to conduct cost-benefit analyses on rules deemed “economically significant,” which are defined as having an annual effect on the economy of at least $100 million. The Congressional Research Service, therefore, has warned that it is inherently difficult to estimate the total cost of regulations and that estimates “should be used with a great deal of caution”.3

What is clear is the Trump administration is serious about reducing regulatory burdens businesses face. It has done so by instituting a freeze that has slowed the number of new regulations considerably and by reinterpreting existing statutes to be more favorable to business than during the Obama administration. The Trump administration, in turn, has touted its pro-business stance as having contributed to the acceleration in economic growth over the past year to a 3% annual rate from 2% previously.

Most economic analyses have credited the changes in tax legislation that were enacted at the end of 2017 rather than deregulation for this outcome. The consensus view, for example, is the stimulus from corporate and personal tax cuts were front-end loaded and will add the equivalent of 1% to 1.3% of GDP this year. By comparison, the impact on the economy over the long-term is estimated to be 0.1%-0.2% per annum, compared with 0.5% by the Trump administration.

An alternative view is that of Mickey Levey, chief economist for Berenberg Capital Markets, who contends the easing of burdensome regulations has been a key factor driving U.S. business confidence, production, and capital spending: “While the deregulatory thrust has received far less attention than 2017’s tax reform deliberations or 2018’s skirmishes on trade policy, it is of utmost importance to business production processes and decisions about hiring, expansion plans, and investment strategy.” As evidence, Levy cites the latest survey by National Federation of Independent Business (NFIB), which shows that many small businesses have expressed reduced concerns about government requirements, and Levy links this to improved manufacturing sentiment in the ISM survey.

Levy’s forecast for the U.S. economy over the long-term is upbeat: He believes the improved climate for business investment spending will help lift the potential growth rate of the economy from the Fed’s estimate of 1.8% per annum to at least 2% soon. In this regard, Levy contends that a “growing web of regulations imposed at the national, state and local level” after the 2008-09 financial crisis created policy-induced “supply constraints” that offset the Fed’s unprecedented monetary stimulus.4

At this juncture, it is too early to tell which view is correct. However, insofar as improved business sentiment translates into increased business capital spending, there is some corroboration for the view that burdensome regulations impeded economic growth after the financial crisis.

Impact of Environmental Regulations

Because of difficulty quantifying the impact of regulations on the overall economy, I have taken a closer look at two areas — the environment and financial services — where government regulation is especially important.

With respect to the environment, the signature piece of legislation was the Clean Air Act that was enacted in 1970, which authorized the development of comprehensive federal and state regulations from both industrial sources and automobiles. It was followed by amendments to cover geographic areas that do not meet one or more of the federal quality standards in 1977 and legislation enacted in the early 1990s to deal with the problem of acid rain. Considerable progress has been achieved in battling air and water pollution, which has improved human health and the environment.

Nonetheless, a prevalent view today is environmental policy is extremely complex, has led to ungainly bureaucracies, has incurred high costs, is politically polarized and is also very litigious.5 A report by the Brookings Institution on the 30th anniversary of the creation of the EPA, for example, acknowledged that U.S. companies were complaining about the high cost of compliance, and it cited two studies that estimated the annual cost in the late 1990s to range between $144 billion to $185 billion.6 Businesses have also complained the rules have outlived their usefulness, have resulted in job losses, and make American companies less competitive internationally.7

What would better statutes entail? The consensus among experts is policymakers should seek market-oriented solutions to environmental problems. One application is the way Congress dealt with the problem of acid rain with an approach that became known as “cap and trade” because the government sets caps on the total amount of allowances and permits them to be traded between companies that emit sulfur dioxide. Economists favor this approach because it means that the reduction in emissions takes place at plants that can accomplish the goal most cheaply, which is consistent with efficient resource allocation. Also, because allowances command a positive price, firms are incented to reduce their emissions and profit by selling allowances.

By comparison, solutions to global warming have proven to be more difficult to implement in the United States. The main problem in dealing with global warming is that it arises from burning fossil fuels, which is basic to the economy and jobs. To burn less requires either constricting the economy, making it more energy efficient, or providing alternative sources of energy. A proposal to tax carbon emissions has been put forth by a group of former government officials — James A. Baker III, George P. Shultz, and Henry M. Paulson — who contend it is a “conservative climate solution” that is based on free-market principles.8 The proposal would substitute the carbon tax for the Obama administration’s Clean Power Plan, a complex set of regulations that President Trump has pledged to repeal and which is tied up in many court challenges. However, the Trump administration has failed to endorse the carbon tax plan, because it believes it is too costly.

Financial Regulation: Finding the Right Balance

The considerations entailed in the regulation of the financial sector belie its importance to the overall economy and household savings. The history of the nineteenth century is replete with numerous U.S. banking crises that resulted in people rushing to withdraw deposits before banks collapsed, and the worst experience was the 1930s when more than 5,000 banks failed. It resulted in Glass-Steagall legislation, which prohibited commercial banks from participating in the investment banking activities. Glass Steagall is generally credited as contributing to financial stability during the post-war period when banking crises were few and far between. Nonetheless, several factors coalesced to bring about its repeal as financial markets were liberalized around the world beginning in the 1980s and continuing into the late 2000s.

The case for increased regulation undertaken by the Obama administration was that the Global Financial Crisis (GFC) was a consequence of market failure. This view was the majority opinion of the Financial Crisis Inquiry Commission (FCIC) that was formed to investigate the causes of the crisis and to make recommendations to enhance the safety and soundness of the financial system. The origins of the crisis were attributed to a bubble in housing and a breakdown in the process of securitizing mortgages: “It was the collapse of the housing bubble –fueled by low-interest rates, easy and available credit, scant regulation, and toxic mortgages — that was the spark.”9 The severity of the crisis, in turn, was attributed to failures of corporate governance and risk management at many systemically important financial institutions.

For some observers, the FCIC’s findings are moot, because Congress already had passed the Dodd-Frank Act six months before the report was released. At first blush, many of the goals of Dodd-Frank seem laudatory: providing better consumer protection from abusive financial practices, ending bank bailouts, creating an early warning system, and improving transparency and accounting for exotic instruments. However, many observers are skeptical that Dodd-Frank can produce the desired results. Among the principal criticisms are the following:

- The bill is too complex. It contains 849 pages of legislation and several thousand pages in subsequent rule-making documentation.

- It has proved to be very costly with uncertain benefits. A study by the American Action Forum concluded that at the end of its sixth anniversary Dodd-Frank had imposed more than $36 billion in cost on the financial services industry and 73 million hours of paperwork.10

- It imposes significant new restrictions on activities of many banks, insurance companies and other financial institutions that had little to do with the crisis. As a result, it could result in regulatory overkill.

- It is unlikely to protect against the next financial crisis. One of the key objectives of Dodd-Frank, for example, is to mitigate the risk of “Too Big to Fail.” However, Charles Calomiris of the Columbia Business School contends the provision to provide for the orderly liquidation of insolvent institutions is unworkable, and that the path of least resistance remains bailouts.11 Furthermore, the banking industry has become even more concentrated since the GFC, with the top five U.S. banks today accounting for nearly one-half of all deposits, as compared with 30% before the crisis.

What can be done to address these issues? Views on this matter are diverse depending on the perspective about the factors contributing to the financial crisis and possible remedies. The approach the U.S. Treasury has advocated would redress what it sees as a problem Dodd-Frank has created: Namely, it contends Dodd-Frank has discouraged banks from extending credit to small businesses and that it has created “an excess of capital.”

In reviewing these issues, however, some observers have challenged Treasury’s claim that regulations have resulted in slower growth of credit.12 While it is often asserted that banks have been constrained from making loans to small businesses due to restrictions, the Fed’s quarterly survey of senior loan officers does not point to an unusual pattern of credit tightening since Dodd-Frank was enacted.

The biggest changes under consideration by the Treasury would alleviate capital and liquidity requirements for the largest banks. According to the U.S. Treasury, there is now an “excess of capital” that constrains the supply of bank credit, and it calls for a “recalibration” in cases where regulators have set requirements on the largest U.S. banks that are in excess of international standards. Yet the institutions that became troubled during the GFC were ones that sought to boost overall profitability via excessive financial leverage and which funded the purchase of illiquid instruments with short-term borrowings. The trigger for disaster was the value of their assets plummeted when the housing bubble burst and the impact were magnified by the need to de-lever their balance sheets quickly at fire-sale prices.

The bottom line is that while there is a strong case for lessening the regulatory burden of Dodd-Frank, there is also a risk the pendulum could swing back too far in the direction of lessening capital and liquidity requirements, which would leave the financial system exposed to unforeseen risks.

Implications for Financial Markets

The Trump administration’s efforts to deregulate the economy is often cited as a factor that has buoyed the stock market. However, it is difficult to quantify the overall market impact for the same reason that it is hard to quantify the impact on the overall economy.

What is evident is the GFC and its aftermath proved to be a toxic environment for bank stocks and other financials. As a group, the financial sector materially underperformed the broad market from the onset of the crisis in 2008 until the November 2016 election (Figure 2). This reflected a combination of forces including the profitability of financial institutions being crushed by losses on holdings of securities and loans, record low-interest rates and narrow credit spreads, and increased regulatory burdens imposed by Dodd-Frank. In fact, many investors concluded that the aim of the regulations was effectively to make financial institutions behave more like regulated utilities, and financial stocks trailed the broad market.

In the aftermath of the 2016 election, financial stocks surged initially through the end of 2016 and then performed in line with the broad market during 2017 for the first time in nearly a decade. This partly was due to the perception that the Trump administration would seek to roll back Dodd-Frank, while also lessening regulatory oversight of financial institutions. In addition, financial stocks benefitted from expectations that stronger growth would enable the Federal Reserve to begin normalizing interest rates. Although financials underperformed in the second quarter of 2017, as investors perceived the Fed would slow the pace of policy tightening, the sector still finished the year 19% higher, which was in line with the broad index. Looking ahead, it is generally agreed the performance of financial stocks is closely tied to the performance of the economy and to the path of interest rates.

This commentary is a distillation of a chapter in Nick Sargen’s “Investing in the Trump Era: How Economic Policies Impact Financial Markets” published by Palgrave MacMillan in July 2018.

1 See Mickey Levy commentary for Berenberg Capital Markets, “Chart of the week – U.S. deregulation drives momentum in business and economy,” June 29, 2018.

2 “The Impact of Regulatory Costs on Small Firms,” SBA, September 2010.

3 See The Congressional Research Service, March 27, 2017.

4 See Mickey Levy op. cit.

5 See Donald F. Kettl, “Environmental Policy: The Next Generation,” The Brookings Institution, October 1, 1998.

6 Ibid.

7 The problems, to a large extent, stem from the Clean Air Act being one of the first in a series of statutes that gave citizens the right to regulatory protection, to command agencies to do what is necessary to protect those rights, and to direct courts to enforce the demands. During the 1970s, consumers and environmental groups also began to receive “intervention” or “public participation” funding to cover their costs for advocating before federal agencies in the public interest.

8 John Schwartz, “A Conservative Climate Solution: Republican Group Calls for Carbon Tax”, The New York Times, February 7, 2017.

9 The Financial Crisis Inquiry Report, submitted by The Financial Crisis Inquiry Commission, January 2011, Official Government edition.

10 Sam Batkins, Dan Goldbeck, “Six Years After Dodd-Frank: Higher Costs, Uncertain Benefits,” American Action Forum, July 20, 2016.

11 Charles W. Calomiris, “Four Principles for Replacing Dodd-Frank,” The Wall Street Journal, June 16, 2017.

12 See Kim Schoenholtz, Money, Banking and Financial Markets, “The Treasury’s Missed Opportunity,” June 19, 2017.