- Emmanuel Macron’s election as President of France has buoyed European markets, as it is the third election this year in which populist candidates have been defeated. Moreover, with Angela Merkel’s party scoring key wins in regional elections, her chances of being re-elected in the fall are high.

- In addition to lessened political risks, investors have been attracted by better-than-expected economic performance in the European Union (EU) this year. Germany’s economy has been the locomotive, and Macron’s election has raised hopes that France will finally embark on much-needed structural reforms and that a renewed Franco-German partnership will revive the EU, as well.

- Weighing these considerations, this may be a good time to add exposure to European equity markets: Profit growth has surged recently and political risk has lessened, while the discount on European stocks relative to the U.S. is in line with long-term norms. The main risks are that Macron may not be able to deliver reforms and a populist leader could become Italy’s next President.

Background: EU Political Risks Lessen, While European Economies Improve

At the start of this year, a key issue relating to Europe was the prospect that elections in several countries—notably, Austria, Holland, France, Germany, and Italy—could result in populist victories that would threaten the EU’s viability in the wake of last year’s vote in the UK in favor of Brexit. France’s election was perceived to be the most important, because Marine Le Pen, the far right candidate, advocated that France should leave the EU and the euro. While the odds of this happening were low, investor concerns heightened leading up to the first round elections, when there was a possibility Le Pen and far-left candidate, Jean-Luc Mélenchon, could be the two finalists. In the event, Emmanuel Macron, a centrist politician who campaigned as a reformer, emerged as the front runner and went on to defeat Le Pen handily in the run-off.

In the wake of these developments, European equity markets rallied at one point by 5%, led by an 8% advance for the CAC. The rally not only reflects investor relief that France will remain a core member of the EU, but also that the tide of populism on the continent has been contained: The French election is the third in a row in which populist candidates were defeated, and recent state elections in Germany indicate that Angela Merkel’s prospects for being re-elected Chancellor appear very good.

At the same time, the EU has experienced better-than-expected economic performance, led by Germany: The 2.5% annualized rise in German GDP in the first quarter was the biggest in four quarters, and was well above potential (1.8% according to European Commission estimates.) Investment in machinery and equipment also picked up in the quarter, suggesting a broadening of the expansion, which had been led by personal consumption. German GDP in real terms is now 8.5% above its pre-crisis peak in 1Q 2008, well above other EU members. Meanwhile, unemployment in Germany has fallen below 4% from a peak of more than 10% during the crisis.

For the EU as a whole, real GDP growth was 2% annualized, the best showing in the past two years. The improvement in growth is linked to the European Central Bank’s policies to keep interest rates near zero while expanding its balance sheet via asset purchases. In addition, the 10% depreciation of the euro against the dollar in the past three years helped boost exports.

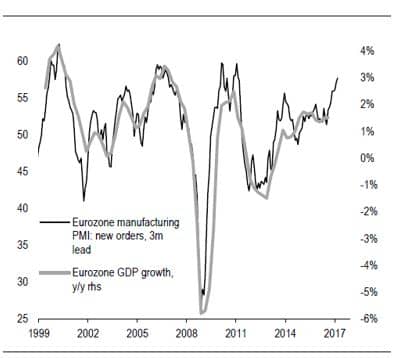

As in the United States, so-called “soft data” such as purchasing managers’ indexes and sentiment readings show a marked pick-up since the latter part of 2016. Indeed, according to Credit Suisse, the latest PMI readings are consistent with EU growth accelerating to 3% (Figure 1). We would note, however, that hard economic data does not yet indicate the improvement in business sentiment. Nonetheless, the latest EC forecast calls for the EU to grow by 1.7% this year, which is a considerable improvement from the past few years.

Figure 1: European PMI Surveys Point to Stronger Growth

Source: Thomson Reuters, Markit, Credit Suisse.

Source: Thomson Reuters, Markit, Credit Suisse.

Another positive development is headline CPI has accelerated this year and is approaching the ECB’s 2% target, after running close to zero in 2015-2016. This suggests the threat of deflation is waning, and the ECB can consider normalizing interest rates if this pattern continues. That said, we believe the ECB will be very cautious about tightening monetary policy.

Will Macron Transform France & the EU?

To some extent, the boost in European equities since the first round of the French elections can be attributed to a relief rally that Marine Le Pen was not elected. Beyond this, in the wake of Macron’s very decisive victory, some observers have asked whether the election could represent a turning point for France and the EU: Macron is a reformer who also seeks closer ties between France and Germany, which constitute the core of the euro-zone.

Soon after his election, Macron visited German Chancellor Angela Merkel, and both pledged to work closely to draw up a “road map” of reforms for the EU, including the possibility of implementing treaty changes, if necessary. Merkel noted that work first needed to be conducted on reforms that are needed before changes in the EU treaty would be implemented. One of the most important is the need for greater fiscal sharing if the EU is to evolve from a monetary union to a fiscal union. To go down that route, however, Germany wants to be confident France is committed to structural reforms that will make its economy more dynamic. The reason: Germany undertook a comprehensive set of labor market reforms in the previous decade that are credited for reviving its economy.

For his part, Macron has called for a “revolution” to simplify France’s Labor Code, which is a 3,600 page document that regulates nearly every aspect of employer-employee relations. This will not be easy to pull off, however, as he will encounter strikers and protesters, as previous French Presidents have. For example, Francois Hollande, Macron’s processor, backed away from embarking on labor reforms in the face of stiff opposition. Other reforms being considered include cutting the corporate tax rate from 33% to 25%, and reducing the size of France’s bloated government. The latter goal, however, is modest, as Macron seeks to slow the expansion of government rather than to reduce its size, which is the largest among the leading industrial countries.

Having formed a new political party, Macron must first build a coalition with existing parties, so that he can gain a legislative majority in the parliamentary elections in June. Those he has recruited so far lean strongly to the left, with many coming from the reform faction of the Socialist Party. To appeal to the right, Macron is credited with making a wise choice of Édouard Philippe as Prime Minister. Still, it appears unlikely Macron will win an outright majority, and he therefore may have to rule with a coalition. Consequently, it remains unclear how successful he will be in achieving reforms that France desperately needs.

The Case for European Equities

The principal reasons for considering European equities are that (i) earnings prospects have improved with the economic upturn, while (ii) Macron’s election and the rejection of populism in several key European countries have lessened political risk.

The improvement in European corporate profits is shown in Figure 2. It illustrates how far they lagged the U.S. market when economic growth trailed that in the U.S., and how they have improved recently. Among developed countries, European stock markets traditionally have been the most levered to economic performance, and this continues to be the case, as earnings growth in Europe has exceeded that in the U.S. recently. Moreover, the percentage of European companies beating expectations is the highest in a decade. An additional factor supporting corporate profitability has been the weak euro. Although it has firmed against the dollar recently, it is still relatively cheap on a purchasing-power basis.

Figure 2: European Corporate Profits Lag the U.S. Until Recently

12-month trailing EPS, Index, Jan 2006 = 100

Source: Datastream, JPMAM. April 28, 2017.

Source: Datastream, JPMAM. April 28, 2017.

On the surface, it appears European equities may offer good relative value, as the discount of European multiples to the U.S. is about 15%. The latter, however, is close to the average of the past decade or so, when one takes into account differences in the sector compositions. Therefore, we consider European equities to be reasonably valued relative to the U.S.

The other major consideration is that political risk in Europe has diminished considerably with Macron’s election and the likelihood that Angela Merkel will be re-elected Chancellor of Germany. This has contributed to inflows of funds into European markets recently. The principal risk for investors is disappointment that Macron may not be able to deliver on his reform agenda. Another risk is that populism could resurface in the Italian presidential elections that must be held no later than a year from now.

Weighing these considerations, I believe now may be a good time to add to European equities, after years of being cautious about European markets.